Founders keep asking me a binary question: US or EU? After building Dronehub across both for a decade and now starting Oswin AI on the US side, my honest answer is that the binary is the mistake. You don't pick a continent. You assign functions to continents.

Here's the thesis in one line: build and run your R&D where the engineering talent and the non-dilutive funding are — that's Europe — and raise your growth capital and sell into the largest single market — that's the US. I didn't arrive at this from a slide deck. I arrived at it by doing the wrong version first, paying for it, and correcting.

Why I treat "US vs EU" as the wrong question

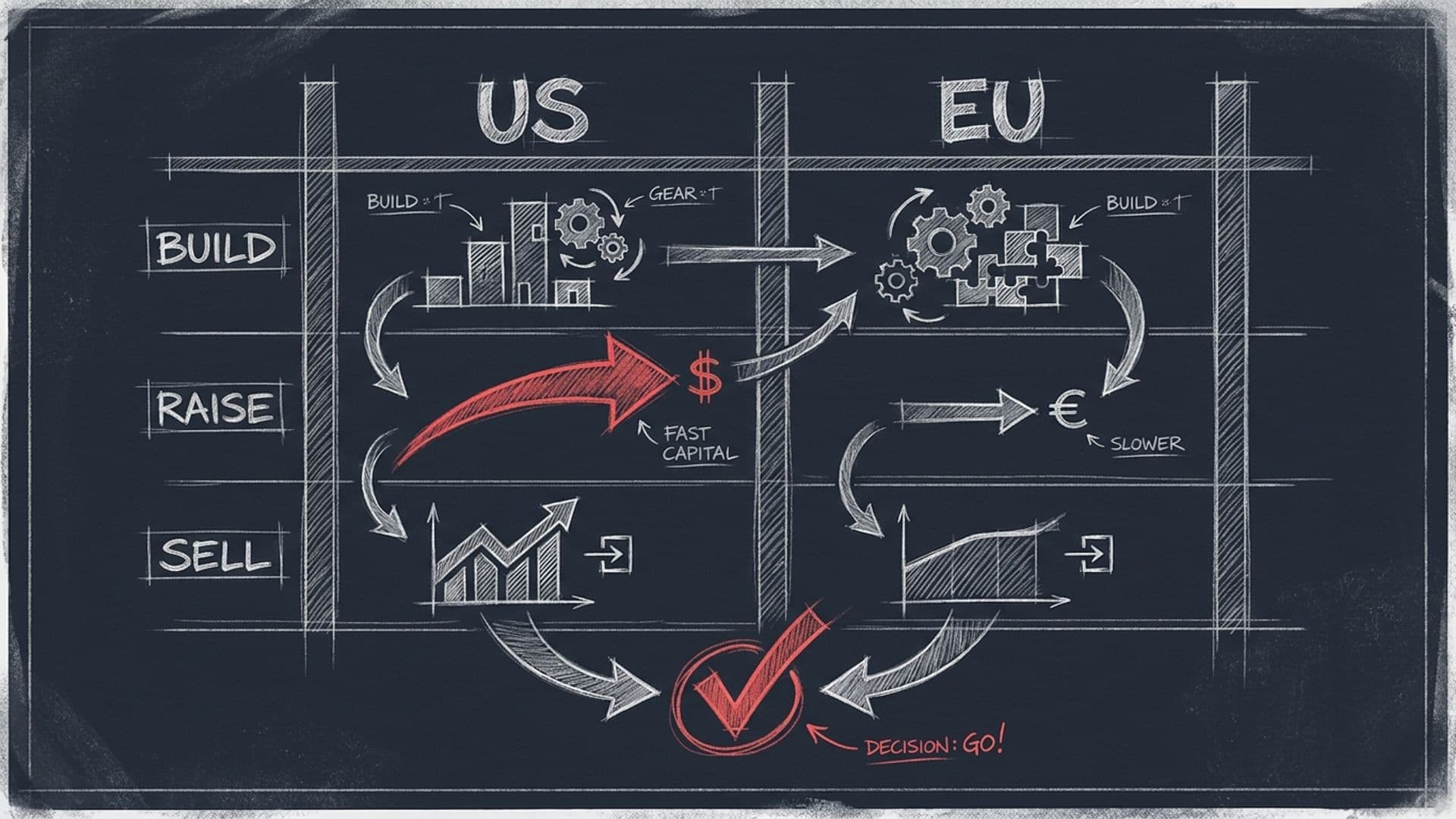

When you frame it as a choice, you're assuming one geography has to win on every axis: talent, cost, capital, regulation, customers, speed. None does. The US is unbeatable for market size and growth capital. Europe is genuinely strong on deep engineering talent and — the part founders underrate — non-dilutive R&D money. The moment you accept that the advantages are split, the decision stops being "where do I incorporate" and becomes "which function goes where."

A deep-tech company really has four geography-sensitive functions: where the legal HQ sits, where R&D actually happens, where you raise, and where you sell first. Most founders collapse all four into one decision because it feels cleaner. It isn't cleaner. It's one decision made badly four times. I'd rather make four decisions well, each anchored to a real, nameable advantage.

If I had to compress the framework into a table:

The rest of this piece is how each row actually played out, with real numbers where I have verified ones.

What Europe gives you: talent and money you don't dilute for

The thing American founders don't fully internalize about Europe is the non-dilutive funding. In the US, early R&D is mostly paid for with equity — you raise, you burn, you raise again, and every round costs you ownership. In Europe there's a parallel system that will pay for hard engineering work and take none of your cap table.

We lived inside that system. Dronehub coordinated a Horizon 2020 project called HUUVER, and we ran a project called AUDROS with both the European Space Agency and the European Defence Agency. These aren't vanity logos. They're how you fund a multi-year, capital-intensive autonomous-systems roadmap without handing investors a third of the company to do it.

The turning point came earlier, in 2017. ESA reached out to roughly fifty European drone companies about an autonomous battery-swap problem — the unglamorous, genuinely hard part of making a drone-in-a-box system run without a human in the loop. We were the one that responded, and we won a contract worth around €200K. That contract did two things. It paid for real R&D, and it gave us a credential that opened the next door, and the one after that. In Europe, an ESA contract is a signal the whole ecosystem reads. It's the kind of validation that's hard to manufacture and harder to fake.

And the talent. The engineers who can build autonomous robotics — control systems, computer vision, the mechanical work of a docking station that swaps a battery in the rain — are dense in Europe and affordable relative to their skill. We built JFACTORY, our precision-manufacturing arm, in Poland for exactly this reason: when your engineers and your CNC machines and your fiber laser sit in the same building, the loop between "design it" and "hold the part" is hours, not weeks. For a hardware company, that iteration speed is the whole game.

If you're a deep-tech founder, the European read is simple: this is where you build the thing. The grants are real, the talent is real, and you can get a long way on capital that costs you no equity.

What the US gives you: one market and capital velocity

Now flip it. Europe is strong on inputs — talent and grants. The US is strong on outputs — market and capital.

Europe is not one market. It's a couple dozen of them, each with its own language, procurement culture, and regulatory texture. Selling into Germany, France, and Poland is three sales motions, not one. The US is the opposite: the largest single market on earth, broadly one regulatory frame, one language, one set of buying norms. For a company trying to scale revenue, that homogeneity is worth an enormous amount. You build the sales playbook once and it travels.

The capital side compounds it. American growth investors are simply more comfortable with hard-tech and robotics risk, they write larger checks, and they move faster. I'm deliberately not going to throw a fundraising number or a valuation at you to "prove" this — those figures get misquoted, and I'd rather you trust the mechanism than a headline. The mechanism is real: capital velocity on the US side is higher, and for a deep-tech company that needs years of runway before it's cash-generative, velocity matters as much as price.

We made the US entry concrete in 2022 through GENIUS NY in Syracuse, where we were a $500K finalist. GENIUS NY is an accelerator built specifically around unmanned systems and autonomy, which made it the right door rather than a generic one. It gave us a US footing, a US network, and a reason for American investors and customers to take a meeting. I've written about that entry in detail in Entering the US Market via GENIUS NY — if you're planning a US landing, that's the operational version of this section.

The other thing that unlocked the US side for me personally was status. In 2024 I got an EB1A "extraordinary ability" green card, which means I can operate and build in the US directly, without being tethered to a visa or a sponsor. I won't soften how much friction that removes. A foreign founder running a US company on a fragile visa is making every decision through an immigration lens. Solving that early was one of the highest-leverage moves I made — the application ran about 1,300 pages, and it was worth every one.

How to run one company across two continents without it falling apart

The obvious objection to all of this is cost. Two geographies, two legal structures, two payrolls, two time zones — isn't that expensive overhead bolted onto a startup that can't afford it?

It is, if you split it wrong. The expensive version is when you duplicate the same function in two places: an R&D team in Europe and a second R&D team in the US, a sales team here and a redundant one there. Then you're paying twice for one capability and your overhead eats the advantage.

The framework only works because each continent owns a distinct function. Europe owns R&D, manufacturing, and the EU grant relationships. The US owns growth capital and the primary sales market. There's almost no overlap, so you're not paying twice — you're paying once for each side's specific advantage. The European cost center produces the technology and the credentials; the US cost center produces the capital and the revenue. They're complementary, not redundant.

It's still hard. Two time zones, two legal systems, the genuine management tax of a team that doesn't all sit in one room. I've written separately about the operational reality of running one company across two continents — the coordination cost is real, and I won't pretend it's free. But the alternative — forcing everything into one geography to keep it "simple" — means giving up either the European grants and talent or the US market and capital. That trade is worse than the coordination tax. You'd be swapping a real structural advantage for an org-chart convenience.

Why Oswin AI starts on the US side — and what that says about sequencing

Here's where my own framework gets interesting, because my new company breaks the pattern — on purpose.

Oswin AI, which I founded in 2026 at the intersection of AI and robotics, is based in the United States from day one. After a decade of building the European way first and bolting the US on second, why start the next one on the US side?

Because the inputs changed. With an EB1A green card I already have unrestricted US status — the immigration friction that made an early US presence painful is gone. And the center of gravity for the kind of AI-plus-robotics work Oswin is doing — the capital, the talent willing to bet on frontier robotics, the customers — is more concentrated on the US side now than it was when I started Dronehub in 2015. The framework didn't change. The weighting of the inputs did. I detail the full reasoning in Why I'm Building Oswin AI in the US.

That's the real lesson about sequencing. The right starting geography depends on which advantage you most need first and which constraints you've already cleared. With Dronehub, I needed non-dilutive R&D money and European engineering talent before anything else, so Europe came first and the US entry came years later through GENIUS NY. With Oswin, the binding constraint is different, so the sequence flips. Same framework, different first move.

What this means and where I'd start

If you're a deep-tech founder staring at the US-vs-EU decision, stop trying to win it as a single choice. Map your four functions — HQ, R&D base, fundraising market, primary sales market — and ask, for each, which geography gives you a real, nameable advantage. Not a vibe. A specific thing: a grant program, a talent pool, an investor base, a market's size.

Concretely, where I'd start:

- Anchor R&D where your talent and your grants are. For most hard-tech, that's Europe. Go find the relevant Horizon Europe, ESA, or EDA programs before you raise a dollar of equity — non-dilutive money is the cheapest capital you'll ever touch.

- Build a thin but legitimate US presence for capital and sales. A real entity, a real network, a real reason for American investors and customers to engage. An accelerator like GENIUS NY can be that door if it fits your domain.

- Solve your own status early if you intend to be hands-on in the US. The EB1A path is brutal, but it ends the visa dependency that quietly distorts every other decision.

- Sequence by your binding constraint. Whatever you most need first — grants, talent, capital, market — go get that first. The order isn't fixed; the principle is.

I've now done it both ways: Europe-first with Dronehub, US-first with Oswin AI. The continent was never the answer. The function was. Assign each one to the geography that actually earns it, and the map stops being a fork in the road and starts being a tool. If you want to compare notes on a specific build, reach out.

Key facts

In 2017, the European Space Agency reached out to around 50 European drone companies about an autonomous battery-swap problem; Cervi Robotics (now Dronehub) was the one that responded and won a contract worth roughly €250K.

Source · Dronehub company history; ESA contract, 2017

Dronehub coordinated the Horizon 2020 HUUVER project and ran AUDROS with the European Space Agency and the European Defence Agency — all EU non-dilutive R&D funding sources.

Source · site.ts companiesLed; Horizon 2020 / ESA / EDA

Vadym Melnyk's company was a $500K finalist at GENIUS NY in Syracuse, New York, in 2022, marking its formal US market entry.

Source · site.ts recognition; GENIUS NY 2022

Vadym Melnyk holds a US EB1A 'extraordinary ability' green card, granted in 2024; the application ran about 1,300 pages.

Source · site.ts; EB1A green card, 2024

Vadym Melnyk founded Oswin AI in 2026, a company at the intersection of AI and robotics based in the United States — a deliberate US-side bet.

Source · site.ts ventures; Oswin AI, founded 2026

Dronehub was founded in 2015 as Cervi Robotics and rebranded to Dronehub in 2020; it is a Financial Times FT1000 company (2023).

Source · site.ts; FT1000 2023

FAQ

- Should a deep-tech founder choose the US or the EU for their headquarters?

- My answer is that the question is wrong. You don't choose one continent for everything — you assign functions. I run R&D in Europe because that's where the engineering talent and the non-dilutive funding from ESA, the EDA, and Horizon Europe live. I raise growth capital and sell into the largest single market from the US side. Pick the geography per function, not for the whole company.

- Why build deep-tech R&D in Europe instead of the US?

- Two reasons: talent density and non-dilutive money. European programs like Horizon Europe, ESA, and the European Defence Agency will fund hard engineering work you'd otherwise have to dilute equity to pay for. We built our autonomous battery-swap system on a roughly €250K ESA contract in 2017. That's grant money that bought us real R&D without selling a piece of the company.

- Why is the US better for raising growth capital and selling?

- The US is the largest single market with one language, one broadly aligned regulatory frame, and a deep pool of growth investors who write big checks fast. In Europe, scaling means crossing borders, languages, and procurement regimes. We entered the US through GENIUS NY in 2022 as a $500K finalist. The point of being on the US side is reach and capital velocity, not lower cost.

- Do you need a US green card to build in the United States as a foreign founder?

- You don't strictly need one to start, but it removes enormous friction. I got an EB1A 'extraordinary ability' green card in 2024, which lets me operate and build directly in the US without visa dependency. If you're serious about a US presence, solving your own immigration status early is one of the highest-leverage things you can do.

- Isn't running one company across two continents just expensive overhead?

- It can be if you split badly. The cost comes from duplicating the same function in two places. The framework works when each continent owns a distinct function — Europe owns R&D and EU grants, the US owns growth capital and the primary sales market — so you're not paying twice for the same thing. You're buying the specific advantage each side actually has.

- Where should a founder start if they want to apply this split?

- Start by mapping your four core functions — HQ, R&D base, fundraising market, primary sales market — and asking which geography gives each one a real, nameable advantage. Anchor R&D where your talent and grants are. Then build a thin but legitimate US presence for capital and sales. Don't try to do everything at once; sequence it the way we did, R&D first, US entry second.