If you are building hardware plus AI in Europe and you are waiting for the fundraising story that looks like a US deep-tech profile, you will wait a long time. The European version is grant-heavy, capital-modest, and slower to look impressive on paper. My thesis is simple: in Europe you assemble capital from public programmes and accelerators rather than one large venture round, you usually end up building your own manufacturing whether you planned to or not, and the EU R&D system both funds you and quietly shapes what you build. None of that is a complaint. It is just the terrain, and most founders are not warned about it before they start.

I have lived this with Dronehub, the autonomous drone-in-a-box company I founded in 2015 as Cervi Robotics and rebranded to Dronehub in 2020. What follows is the field guide I wish someone had handed me.

Why European hardtech capital is grants, not a giant round

The first thing to unlearn is the mental model where you raise a Series A, hire fast, and let burn do the work. That path exists in Europe, but for capital-intensive hardware with multi-year development cycles, the early-stage venture market is thinner and more conservative than in the US. Investors who write large checks into pre-revenue hardware are rare, and the ones who exist often want the kind of traction that hardware physically cannot produce on a software timeline.

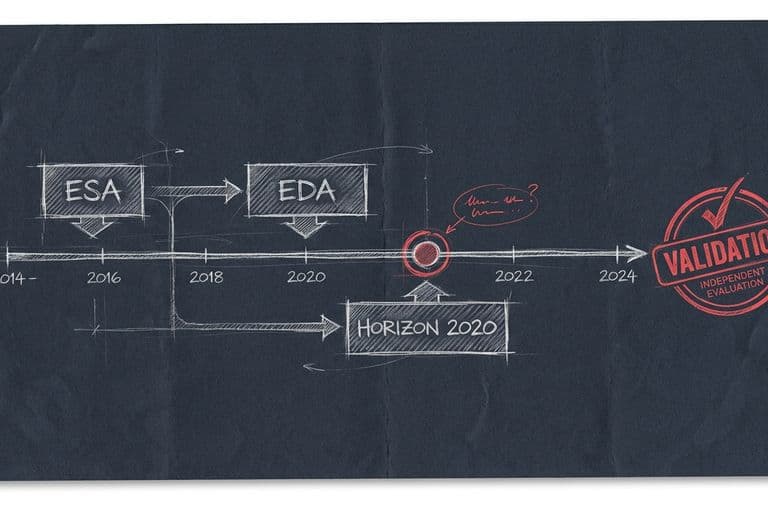

So you do what we did: you stitch capital together from sources that each have their own logic. For Dronehub, that meant an ESA contract in 2017 worth roughly €200K-€250K for autonomous battery-swap work, grants from Poland's NCBR, and the Horizon 2020 HUUVER project, which we coordinated and which carried a total budget of €1.62M with €1.197M in EU funding. Later, in 2022, came the GENIUS NY finalist position in Syracuse, New York: $500K, but through a SAFE, an equity instrument, not a grant.

I am deliberate about that last distinction because founders blur it constantly. A SAFE converts into equity later. It is dilutive capital that simply has not priced itself yet. A Horizon Europe grant or an ESA contract is non-dilutive in the equity sense. Both are real money. They cost you very different things. If you describe your accelerator SAFE as if it were free grant money, you have misunderstood your own cap table, and so will anyone who funds you next.

The honest summary of our capital history is that it was grant- and accelerator-heavy, not a single big VC raise. That is not a failure mode. For a lot of European deep-tech, it is the only viable mode.

The hidden cost of grant capital: time and direction

The pitch for non-dilutive funding is seductive: money that does not touch your equity. The reality has two costs that nobody puts on the slide.

The first is time. A serious Horizon or ESA proposal is a months-long undertaking, often with a consortium of partners you have to assemble and align. Then, once you win, the reporting, audit, and co-financing obligations are continuous. For a small team, the founder is usually the one writing the proposal and the founder is usually the one the product needs that same week. Grant money is cheap in equity and expensive in calendar.

The second cost is direction. Public calls fund specific objectives. When you win HUUVER or an ESA contract, you are committing to build toward what that programme defined, alongside partners who have their own needs. When the call aligns with your roadmap, this is a gift: someone is paying you to build the thing you were going to build anyway, and handing you credibility on top. When it aligns only partially, you spend real engineering hours steering toward deliverables that are adjacent to, but not exactly, your product. Over several grants, that pull is a force you have to actively manage.

I am not arguing against grants. They were genuinely a turning point for us. The 2017 ESA work, in particular, came after ESA reached out to around fifty European drone firms and Cervi was the one that actually answered the call. I have written about that moment separately in The ESA Call, because it changed the company's trajectory. The point is that grants are a real funding instrument with a real price, paid in focus, and you should budget for that price the way you would budget for dilution.

Why you end up building your own factory

Here is the constraint that surprises software-minded founders most: in hardware, you often cannot outsource your way to iteration speed.

The theory says you design the part, send it to a contract manufacturer, and receive finished units. The practice, for low-volume hardware that changes every few weeks, is that the exact parts you iterate on most are the slowest and most expensive to get made externally. Lead times, minimum orders, and the back-and-forth of revisions all fight against the one thing an early hardware company needs most, which is the ability to change the design on Monday and have a new physical part on Thursday.

So we brought production in-house. Not out of vertical-integration ideology, but because the product demanded it. That capability grew into JFACTORY, a precision-manufacturing arm of the Dronehub group in Jasionka, Poland, doing CNC machining, fiber-laser cutting, and 3D printing. It was born directly out of our own drone production. The docking station with its battery-swap mechanism, which sits at the heart of an autonomous drone-in-a-box system, is exactly the kind of precise, evolving mechanical assembly that punishes you for relying on a slow external supply chain. If you want to understand why that mechanism is so central, I covered the engineering tradeoff in Battery Swap vs. Charging and the broader system in What Drone-in-a-Box Actually Means.

There is a second-order effect worth naming. Once you own manufacturing, it becomes an asset in its own right, with its own utilization, its own customers, and its own logic. That is a strength and a distraction at once. The European hardware founder who started a software-style company often wakes up one day running a machine shop too. Plan for it, because it is more likely than not.

The transatlantic bridge nobody warns you about

You can build a credible European deep-tech company without ever leaving Europe. You will struggle to scale one to its ceiling without engaging the United States. The largest pools of growth capital, the deepest enterprise budgets, and many of the most serious dual-use and defense buyers concentrate there. This is not a knock on Europe; it is arithmetic.

For Dronehub, the bridge was the GENIUS NY accelerator in Syracuse, which gave us a foothold in the US market and an upstate New York aerospace ecosystem. Personally, I went further and obtained a US EB1A 'extraordinary ability' green card in 2024, becoming a US permanent resident. I mention the green card not as a trophy but as a structural fact: at some point the founder of a scaling European hardtech company is usually the one who has to physically straddle two continents, two regulatory regimes, and two sets of investor expectations. That straddle has costs of its own, in travel, in legal complexity, and in the simple bandwidth of being the connective tissue between two operations.

If you are building dual-use or defense-adjacent technology, the transatlantic question gets sharper still, because the export-control and procurement landscapes differ meaningfully on each side. I unpacked some of that terrain in Counter-UAS and Dual-Use, Explained. The takeaway: design your corporate and IP structure early with the expectation that a US presence is coming, rather than retrofitting it under deal pressure later.

How EU regulation shapes the product, not just the paperwork

The last constraint is the one founders treat as background noise until it is suddenly foreground: the European regulatory and policy environment, especially around AI and autonomous systems.

I sit on the Council of Poland's AI Chamber, which gives me a direct line of sight into how EU AI policy is forming. That vantage point has made one thing clear: in Europe, regulation is not a downstream compliance chore you handle at launch. For autonomous, AI-driven hardware, the rules about where you can fly, what data you can process, how autonomous a system is allowed to be, and how AI decision-making must be governed are upstream design inputs. They constrain the product architecture itself.

For a drone company this is concrete. Airspace rules, beyond-visual-line-of-sight authorizations, and AI-governance expectations are not footnotes; they determine what is even buildable and sellable in a given jurisdiction. A founder who treats compliance as a final-stage checkbox will rebuild core parts of the system. A founder who reads the regulatory direction early designs for it from the start. The same logic is why I argue that autonomous inspection is fundamentally about taking people out of dangerous environments, a framing that also happens to align with where regulation is pushing, which I wrote about in Why Robots Should Inspect Towers and Refineries.

The EU system, then, is a double bind that is also a moat. The regulatory load is heavier and earlier than in many other markets. But once you have built a compliant, certified, audited autonomous system inside that system, you have something competitors cannot trivially replicate, and you have the credibility that comes from operating inside ESA, EDA, and Horizon programmes. Constraint and advantage are the same coin.

What this means and where I would start

If I were starting a European hardware-plus-AI company today, knowing what I know after a decade of this, here is the short version.

Build your capital plan around a portfolio of public programmes and accelerators, not a single hero round, and be ruthlessly honest about which instruments are dilutive. Budget grant money in calendar time and strategic focus, not just euros. Assume you will bring some manufacturing in-house and that it will become a real operation with its own demands. Design your corporate structure early for the transatlantic step you will probably take, rather than retrofitting it under pressure. And treat EU regulation as an upstream design input, because for autonomous AI systems it genuinely is one.

The European path is slower to look impressive and harder to summarize in a headline number. But it produces companies that are deeply built, hard to copy, and grounded in real engineering and real institutions rather than narrative. That is the version of deep-tech I have spent ten years building, and I would not trade the constraints for a fairy tale. If you want the longer arc of what I got right and wrong along the way, I put it in A Decade in Autonomous Drones. And if any of this is useful for something you are building, get in touch.

Key facts

Dronehub's early capital was grant- and accelerator-heavy rather than a single large VC round, including an ESA contract worth roughly €200K-€250K in 2017 for autonomous battery-swap work.

Source · vadmelnyk-knowledge research notes; ESA Space Solutions Cervi profile

The Horizon 2020 HUUVER project, coordinated by the company (as Cervi Robotics), carried a total budget of €1.62M with €1.197M in EU funding and ran December 2019 to January 2022.

Source · Horizon 2020 / CORDIS HUUVER project record (grant #870236)

Dronehub was a 2022 GENIUS NY finalist in Syracuse, New York, receiving $500K through a SAFE (an equity instrument), not a non-dilutive grant.

Source · GENIUS NY 2022 finalist record; vadmelnyk-knowledge research notes

Dronehub spun up JFACTORY, a precision-manufacturing arm in Jasionka, Poland, offering CNC machining, fiber-laser cutting, and 3D printing, born out of in-house drone production.

Source · vadmelnyk.com site.ts companiesLed

Vadym Melnyk holds a US EB1A 'extraordinary ability' green card granted in 2024, and built US presence in Syracuse, NY via the GENIUS NY accelerator.

Source · vadmelnyk.com verified facts; ventures

Vadym Melnyk sits on the Council of Poland's AI Chamber, giving him direct exposure to the EU's AI policy and regulatory environment.

Source · vadmelnyk.com site.ts boards

Dronehub was founded in 2015 as Cervi Robotics and rebranded to Dronehub in 2020; the same year the company turned down roughly €3M of outsourcing work to focus on its autonomous platform.

Source · vadmelnyk.com verified facts

FAQ

- Why do European hardware startups raise less venture money than their US counterparts?

- The European early-stage venture market for hardtech is thinner and more conservative than the US one, especially for capital-intensive hardware with long development cycles. So instead of one large priced round, European founders stitch together public R&D grants, accelerators, and small equity instruments. In Dronehub's case that meant an ESA contract, NCBR and Horizon 2020 grants, and a GENIUS NY SAFE, rather than a single big VC raise.

- Is EU grant funding actually free money for a startup?

- No. Non-dilutive grants like Horizon Europe or ESA contracts do not take equity, but they cost you time, co-financing, reporting overhead, and a degree of strategic direction. You build toward the call's objectives and the consortium's needs, which is great when they align with your roadmap and a tax when they don't. They are a real funding source, but you pay in calendar time and focus.

- Why did Dronehub build its own manufacturing instead of outsourcing?

- For low-volume, fast-iterating hardware, contract manufacturers are slow and expensive on the exact parts you change most. Dronehub built in-house production to control iteration speed and quality, and that capability eventually became JFACTORY, a precision-manufacturing arm in Jasionka, Poland doing CNC machining, fiber-laser cutting, and 3D printing. The manufacturing arm exists because the product demanded it, not because we wanted to be a factory.

- Why does a European deep-tech founder need a US presence?

- The largest pools of growth capital, the deepest enterprise customers, and key defense and dual-use buyers concentrate in the US. For Dronehub, the GENIUS NY accelerator in Syracuse was the bridge into that market, and personally I obtained a US EB1A 'extraordinary ability' green card in 2024. Most European hardtech founders eventually face this transatlantic step if they want to scale.

- How do EU R&D programmes shape what a startup builds, not just fund it?

- Programmes like Horizon Europe, ESA, and the European Defence Agency fund specific calls with defined objectives, consortium structures, and deliverables. When you win one, you commit to building toward those objectives alongside partners, which shapes your roadmap, your hiring, and sometimes your IP arrangements. That is the trade: real money and credibility in exchange for some loss of pure autonomy over direction.

- What is a SAFE and why does it matter that GENIUS NY's $500K was one?

- A SAFE (Simple Agreement for Future Equity) is an instrument that converts into equity in a future round, so it is dilutive capital, not a grant. The distinction matters because non-dilutive grants and equity instruments have very different costs to the founder. Treating a SAFE as 'free' grant money would misstate the actual capital structure of the company.